Contemplating Solana DeFi #2 - marginfi

Contemplating Solana DeFi #2 - marginfi

Exploring the go-to peer-to-peer lending and borrowing platform on Solana.

The recent growth in interest in the Solana ecosystem foreshadows a changing narrative as a shifts towards speed, scalability and useability. Solana DeFi 2.0 is happening.

Most people do not care about the inner workings and technicalities of traditional finance and banking, never mind decentralized finance.

Solana is primed to become the Layer-1 to facilitate widespread adoption. To draw in the masses, simplicity in DeFi is paramount.

Today we go through Lending and Borrowing on marginfi, outline below:

What is marginfi?

Usage and growth

Lending & borrowing

Assets and the introduction of $LST

Account health mechanism

Points… 👀

A quick disclaimer, I am not affiliated in any way with marginfi. Please DYOR before depositing to ANY defi or crypto application and always use a hot wallet which is not in any way linked to your long term asset holdings.

What is marginfi?

marginfi is an open source hyper-intuitive DeFi application that allows depositors and liquidity providers to borrow and lend Solana-native crypto assets seamlessly.

The platform is designed with security and stability in mind, with transparent interest rates and automated liquidation mechanisms to protect lenders and borrowers.

The platform had its inception actually back in 2021, their first Medium article is dated two years ago on Oct 21 2021 - just before the markets peaked and ultimately came crashing down over the following year.

Check it out here:

Pitched as "A single interface to trade across defi" with a unique value proposition of multilevel integrated automation for lending, borrowing and liquidations to prioritize solvency and platform continuity.

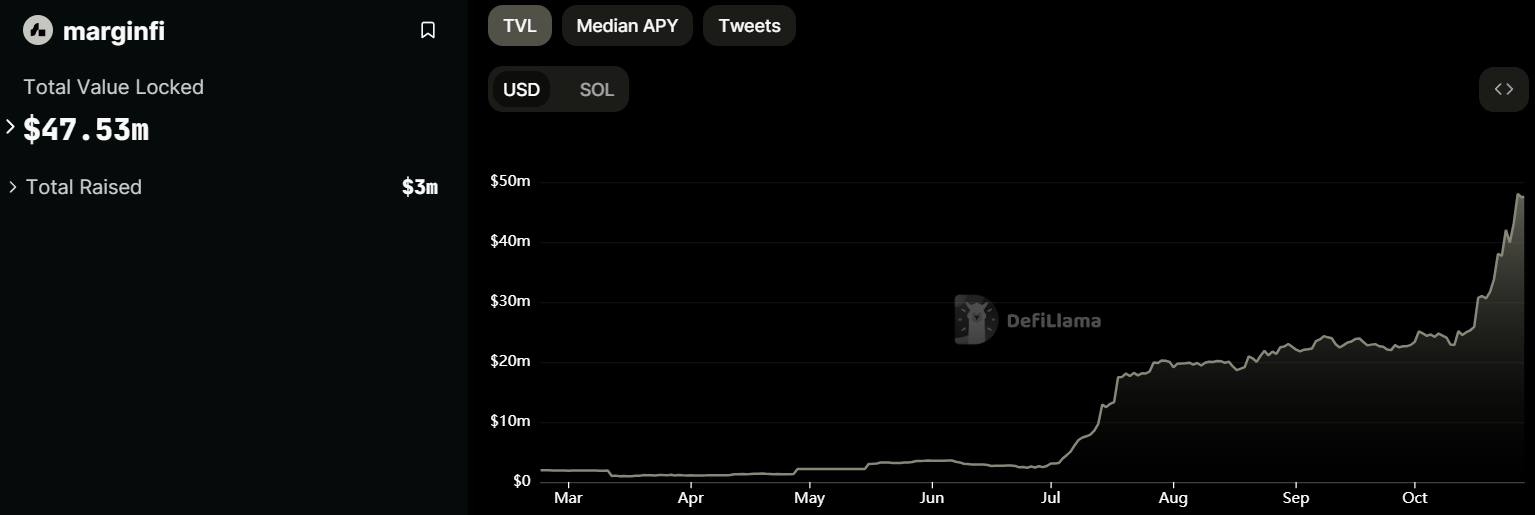

Since then, v2 was announced in May ‘23 which alongside a sense of renewed confidence across the Solana DeFi ecosystem, marginfi seems to have played a big part in spearheading this alongside other aligned teams in the space.

More recently, the daily users and popularity of the platform has exploded. There is clear a correlation between this increase and their announcement of their points program in early July:

Although the TVL of Solana has remained stagnant since FTX, marginfi has seen around a 10x in TVL within 4 months, now sitting at around $50mil - although relatively speaking, this is still incredibly low when compared to L2s and their recent rapid growth.

Lending

You can earn yield by depositing to pools seamlessly without needing to worry about lock up periods or high fees on withdrawals.

Depositors to marginfi earn yields from the fees borrowers incur - currently marginfi doesn’t take a cut of the fees, hence one of the reasons the yields are as attractive as they are.

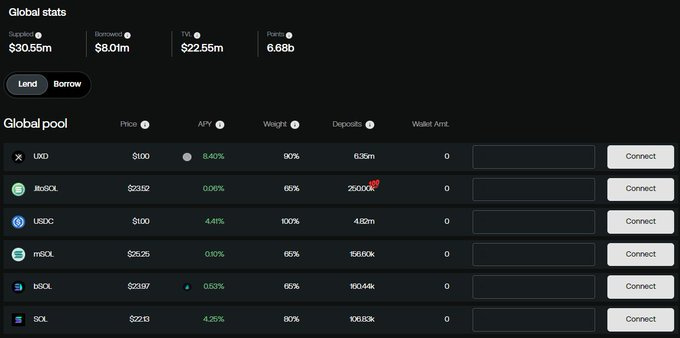

It’s worth noting the the most popular pools are often either close to full capacity or maxed out, so if you want to deposit something like $BONK or $JitoSOL you’ll likely need to wait until the capacity is increased or get lucky waiting for some available space.

Borrowing

By collateralizing your deposited assets, users can borrow funds and take advantage of market opportunities outside of marginfi without being required to sell your crypto holdings.

As a borrower you pay a fee interest on those assets - the rate (APR) depends on what you’re borrowing and the rates fluctuate over time automatically.

marginfi technically enables you to manage something referred to as ‘looping’ where you can essentially rehypothecate any borrowed assets by depositing them again to compound the yields from the APY, this can be repeated until your account ‘health factor’ hits too low a threshold.

Note: This is extremely risky to keep a track of and manage and also increases the risk of being liquidated, but if you have a higher threshold for risk and are seeking significant yield returns this might be something you could stomach.

Liquidations on marginfi are automatically determined if a position falls below the set threshold and the borrower incurs a liquidation fee as a result.

The penalty is 5% of the position of collateral, of which, the fee is split 50/50 between liquidator and the collateral-specific insurance fund.

Assets available

As of today there are currently around 20 crypto assets which are supported.

Assets currently available include the likes of $SOL, $BONK, $HNT and fungible liquid staking derivatives like $JitoSOL (Jito) and $mSOL (Marinade Finance).

$LST:

Most recently there has been a lot of hype and excitement surrounding the release of liquid staking token, $LST - huge brains for the choice of ticker.

This is a collaboration between Jito and marginfi.

The problem:

Native stakers are locked up receiving relatively low yields - there is risk that validators underperform or have varying yields and commissions

Inability for stakers to utilize their $SOL in other applications

Limits in transaction activity on the chain, which limits MEV opportunity - which in turn limits interest and therefore further activity and liquidity flow

The difference between an LSD like $mSOL or $jitoSOL and $LST is that they are managed by many distributed validators with different service levels, fees and commission - resulting in lesser yield in many instances.

$LST is managed by only 3 high performing marginfi validators, but they earn zero commission, and simultaneously all run Jito clients so they compound the APY with the MEV rewards earned, so are able to offer significantly higher yields organically.

The end goal of this is to incentivize holders of Solana natively staking SOL to switch to LSDs to capture more yield and create a higher performing ecosystem through increased transactional activity, liquidity and diversified competition.

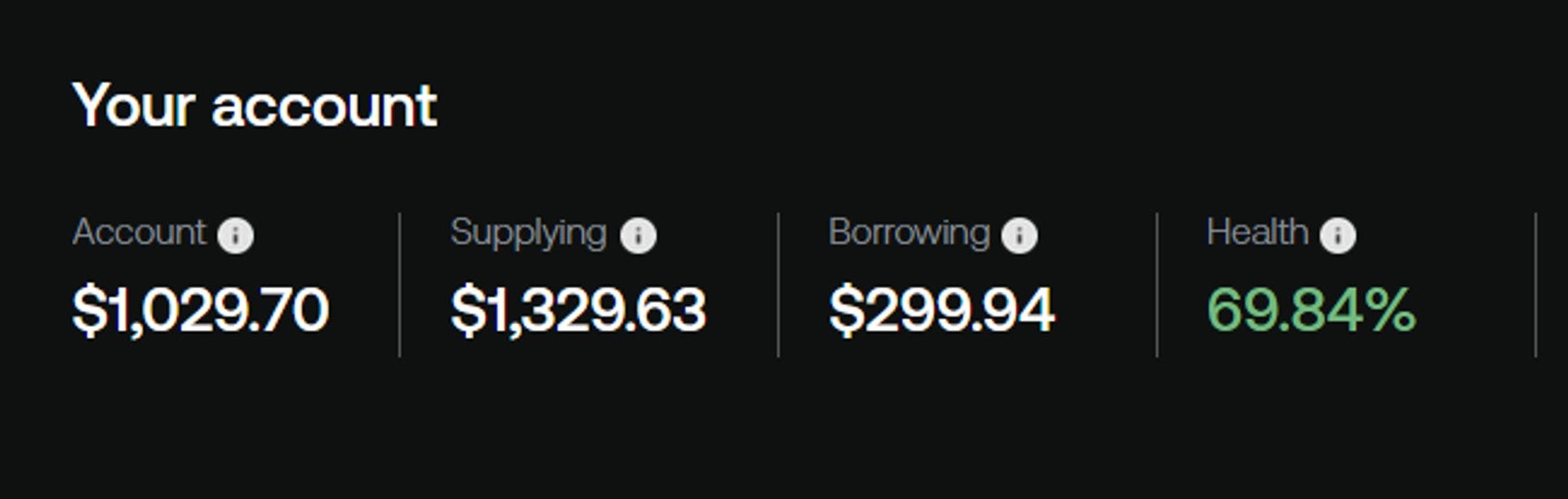

Account health

One of the most important features of marginfi is the health factor, which is determined by the balance of risk in your lending and borrowing portfolio, which is automatically calculated by set formulas.

If you lend on marginfi, you essentially have the option to utilize the loaned assets as collateral and borrow against them.

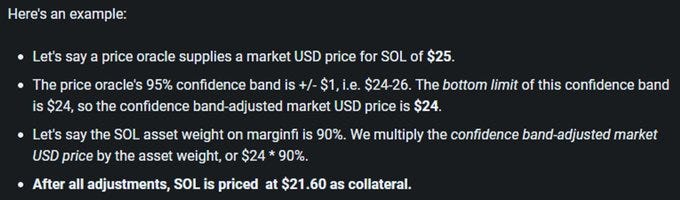

Asset weight:

Available collateral for borrowing is calculated with a weighted mechanism - different for each crypto asset available

The higher the weight - the closer to 100% - the more asset value is available to borrow against

Lesser volatile assets, such as USD denominated stablecoins, retain the highest weighting

See below a good example outlined in the docs and shared below for collateral calculations:

What are points?

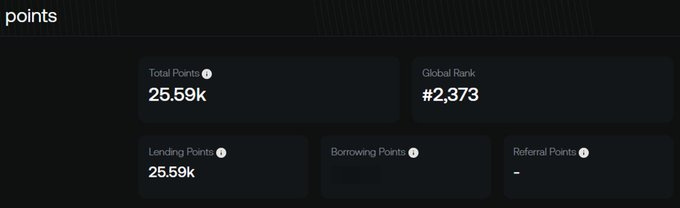

Points-based systems have been popularized recently as a gamified mechanism to incentivize and track engagement and participation within web3 applications.

The more you use the platform the more points you get;

Lending: 1 point per $ per day

Borrowing: 4 points per $ per day

Referrals: earn 10% of new members points, if a member you referred refers someone - you also earn 10% on that referral, so on, so forth

For other applications these points systems determine eligibility for community rewards, or airdrops on token releases.

How rewards will be actually distributed hasn’t been formally confirmed by the MRGN team yet, but its likely the points system is in place to incentivize usage and growth 🪴

It’s an exciting time for Solana DeFi and marginfi will continue to be a pivotal influence in drawing in users and liquidity to the network.

If you want to delve into the platform to deposit and start earning points, I’ve included the link below for you:

I hope you enjoyed this write-up, as usual any feedback appreciated! If you happen to check out marginfi, drop me a comment below or a dm on X to let me know your thoughts, handle:

Thanks for reading!

f.